Energy Gridlock: The Sign of Economic Slowdown?

Global energy issues have caught investors’ attention over the past month. China is rationing electricity, power plants in India are running out of coal and Europeans are paying sky-high prices for natural gas. While North America is in better shape, the global issues are contributing to higher energy prices here, including at the gas pumps. So, how did we get here and will it cause a broader economic slowdown?

The kink in the hose

The reasons for the shortages range from bad luck to bad policies. In Europe, calm winds have curtailed wind turbine electricity supply across the continent, whereas China’s problems stem from their reduction of coal imports from Australia. Other factors include a reduction in coal, oil and gas extraction caused by the pandemic and government policies to combat climate change.

A retro revival?

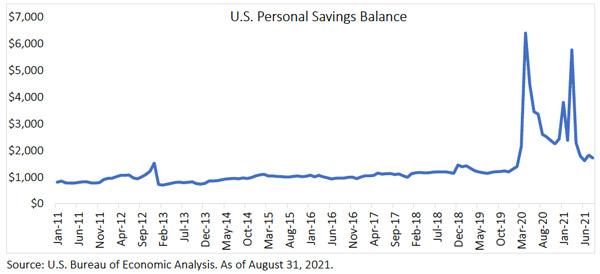

There are concerns that higher energy prices will start to constrain overall consumption and economic growth like it did in the 1970s. In our opinion, the comparisons to the 1970s are not well-founded for a few reasons. Firstly, the share of energy in consumers’ consumption baskets has fallen from 11% in 1960 to just 3% today. Secondly, consumers are still sitting on a pile of savings built up during the pandemic that could be released if the need arises.

The root of the issue

The real reason we don’t foresee a 1970s-like recession is that most of these supply issues are solvable. In Europe’s case, they can import more gas from Russia, although politicians are probably reluctant to approve a pipeline that could be used as a political weapon. In China’s case, they can import more coal to ease the supply crunch. In India, they are ramping up domestic production targets.

In addition, higher energy prices increase the incentives for energy production, which will help balance supply. While we don’t expect a broader economic slowdown due to higher energy prices, we still believe the Organization of the Petroleum Exporting Countries’ (OPEC) supply discipline and recovering demand will keep the price of oil elevated into next year.

Our portfolio positioning on energy

As you know, we take a long-term view when it comes to our positioning strategy but do make tactical adjustments as opportunities arise. Therefore, we continue to hold an overweight position in the energy sector, which has benefitted our portfolio returns. More broadly, our call to overweight equity and simultaneously underweight bonds continues to reward investors. We maintain our core view that the COVID-19 situation will continue to improve, driving a strong recovery across many sectors.

By Alfred Lam, CFA, Senior Vice-President and Chief Investment Officer

By Alfred Lam, CFA, Senior Vice-President and Chief Investment Officer

Marchello Holditch, CFA, CAIA, Vice-President and Portfolio Manager, CI GAM | Multi-Asset Management

This document is intended solely for information purposes. It is not a sales prospectus, nor should it be construed as an offer or an invitation to take part in an offer. This report may contain forward-looking statements about one or more funds, future performance, strategies or prospects, and possible future fund action. These statements reflect the portfolio managers’ current beliefs and are based on information currently available to them. Forward-looking statements are not guarantees of future performance. We caution you not to place undue reliance on these statements as a number of factors could cause actual events or results to differ materially from those expressed in any forward-looking statement, including economic, political and market changes and other developments. CI Assante Wealth Management and its dealer subsidiaries, Assante Capital Management Ltd. and Assante Financial Management Ltd. (collectively “Assante”) are affiliates of CI GAM | Multi-Asset Management, which is a division of CI Global Asset Management. Evolution Private Managed Accounts are managed by CI Global Asset Management under the United Financial brand and are available exclusively through your Assante advisor. Neither CI Global Asset Management nor its affiliates or their respective officers, directors, employees or advisors are responsible in any way for damages or losses of any kind whatsoever in respect of the use of this report. Commissions, trailing commissions, management fees and expenses may all be associated with investments in mutual funds and the use of the Asset Management Service. Any performance data shown assumes reinvestment of all distributions or dividends and does not take into account sales, redemption or optional charges or income taxes payable by any securityholder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. Please read the fund prospectus and consult your advisor before investing. CI Assante Wealth Management is a registered business name of Assante Wealth Management (Canada) Ltd. CI Global Asset Management is a registered business name of CI Investments Inc. This report may not be reproduced, in whole or in part, in any manner whatsoever, without prior written permission of CI Assante Wealth Management. Copyright © 2021 CI Assante Wealth Management. All rights reserved.

Global energy issues have caught investors’ attention over the past month. China is rationing electricity, power plants in India are running out of coal and Europeans are paying sky-high prices for natural gas. While North America is in better shape, the global issues are contributing to higher energy prices here, including at the gas pumps. So, how did we get here and will it cause a broader economic slowdown?

The kink in the hose

The reasons for the shortages range from bad luck to bad policies. In Europe, calm winds have curtailed wind turbine electricity supply across the continent, whereas China’s problems stem from their reduction of coal imports from Australia. Other factors include a reduction in coal, oil and gas extraction caused by the pandemic and government policies to combat climate change.

A retro revival?

There are concerns that higher energy prices will start to constrain overall consumption and economic growth like it did in the 1970s. In our opinion, the comparisons to the 1970s are not well-founded for a few reasons. Firstly, the share of energy in consumers’ consumption baskets has fallen from 11% in 1960 to just 3% today. Secondly, consumers are still sitting on a pile of savings built up during the pandemic that could be released if the need arises.

The root of the issue

The real reason we don’t foresee a 1970s-like recession is that most of these supply issues are solvable. In Europe’s case, they can import more gas from Russia, although politicians are probably reluctant to approve a pipeline that could be used as a political weapon. In China’s case, they can import more coal to ease the supply crunch. In India, they are ramping up domestic production targets.

In addition, higher energy prices increase the incentives for energy production, which will help balance supply. While we don’t expect a broader economic slowdown due to higher energy prices, we still believe the Organization of the Petroleum Exporting Countries’ (OPEC) supply discipline and recovering demand will keep the price of oil elevated into next year.

Our portfolio positioning on energy

As you know, we take a long-term view when it comes to our positioning strategy but do make tactical adjustments as opportunities arise. Therefore, we continue to hold an overweight position in the energy sector, which has benefitted our portfolio returns. More broadly, our call to overweight equity and simultaneously underweight bonds continues to reward investors. We maintain our core view that the COVID-19 situation will continue to improve, driving a strong recovery across many sectors.

By Alfred Lam, CFA, Senior Vice-President and Chief Investment Officer

Marchello Holditch, CFA, CAIA, Vice-President and Portfolio Manager, CI GAM | Multi-Asset Management

This document is intended solely for information purposes. It is not a sales prospectus, nor should it be construed as an offer or an invitation to take part in an offer. This report may contain forward-looking statements about one or more funds, future performance, strategies or prospects, and possible future fund action. These statements reflect the portfolio managers’ current beliefs and are based on information currently available to them. Forward-looking statements are not guarantees of future performance. We caution you not to place undue reliance on these statements as a number of factors could cause actual events or results to differ materially from those expressed in any forward-looking statement, including economic, political and market changes and other developments. CI Assante Wealth Management and its dealer subsidiaries, Assante Capital Management Ltd. and Assante Financial Management Ltd. (collectively “Assante”) are affiliates of CI GAM | Multi-Asset Management, which is a division of CI Global Asset Management. Evolution Private Managed Accounts are managed by CI Global Asset Management under the United Financial brand and are available exclusively through your Assante advisor. Neither CI Global Asset Management nor its affiliates or their respective officers, directors, employees or advisors are responsible in any way for damages or losses of any kind whatsoever in respect of the use of this report. Commissions, trailing commissions, management fees and expenses may all be associated with investments in mutual funds and the use of the Asset Management Service. Any performance data shown assumes reinvestment of all distributions or dividends and does not take into account sales, redemption or optional charges or income taxes payable by any securityholder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. Please read the fund prospectus and consult your advisor before investing. CI Assante Wealth Management is a registered business name of Assante Wealth Management (Canada) Ltd. CI Global Asset Management is a registered business name of CI Investments Inc. This report may not be reproduced, in whole or in part, in any manner whatsoever, without prior written permission of CI Assante Wealth Management. Copyright © 2021 CI Assante Wealth Management. All rights reserved.